How Financial Services Teams Identify Their Best Prospects

Learn how financial services teams can navigate digital transformation challenges, target accounts effectively, and drive ROI with personalized engagement

Post updated on May 7, 2024

The many challenges involved in introducing new technology are well-known to financial services teams. There are already so many legacy systems and applications that, over time, your technology stack can look like a Frankenstein monster of bolted-on parts that don’t always “play nice” with each other. Pull out the much-reviled DOS-based quoting tool and replace it with an AI-fueled app and who knows what might happen next.

Yet something needs to change with your IT infrastructure because customer expectations for digital-first engagement are only growing, and financial service organizations need to keep pace.

Recent history, especially the digital-first acceleration propelled by the global COVID-19 pandemic, has catapulted your buyers forward by several years to a full decade, technologically speaking. Despite all the proliferating legacy systems, today’s financial service firms need to drive digital transformation to keep up with an increasingly digital business landscape marked by higher customer demands for superior digital engagement.

There’s no choice but to adapt, because your customers demand it and your competitors are already driving their own digital transformations. Yet there is good news: Your firm’s digital transformation need not happen overnight, but can start with baby steps (i.e., pilot programs). Nor must it occur evenly.

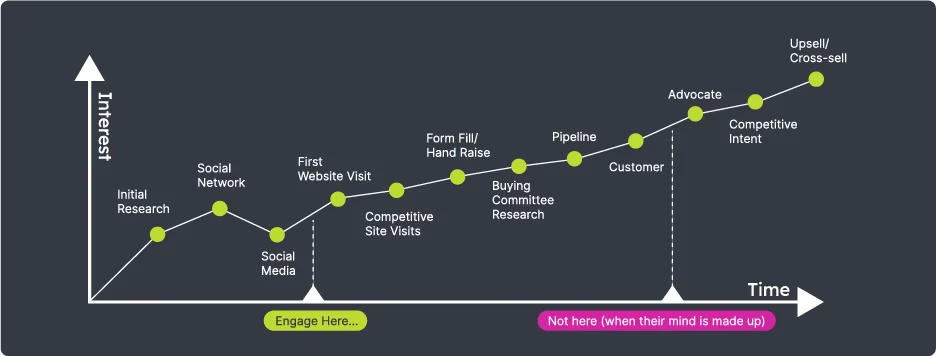

Any financial services Marketing or Sales team can transform itself into a center of excellence without much budget thanks to an account-based pilot. One of the easiest ways to begin is by simply identifying your in-market accounts, the accounts most likely to buy from you as revealed by intent data. When you begin by knowing what to aim at (in-market accounts showing buying intent), you’re more likely to reach your target, optimize your limited marketing and sales resources, and convert an account’s buying intent signals into actual sales revenues.

Start with a target account scoring model

Most of your buyers’ research now occurs online—whether they’re institutional investors or risk officers looking for insurance—and it happens long before they ever reach out to you directly. That means financial firms that build digital capacities gain visibility into what their prospects/target accounts are doing and are thus better able to identify the companies and individuals most likely to buy from them than.

You become proactive in engaging accounts when they’re in-market, rather than waiting (and hoping) they’ll reach out to you directly.

In the recent past, all financial services firms could do was blanket the market in full-bleed print ads. That’s a generic, undifferentiated approach to engagement called “spray and pray.” It’s like walking around outside wearing a sandwich board that says “pick me!” You might hit the mark on occasion with some prospects, but you’re much more likely to miss the mark because you don’t know who the mark is. Now, you can dump the sandwich board and pick your targets proactively and with precision, based on data and science that shows what your accounts/prospects need.

What this means in practical terms is that financial marketers that identify their in-market accounts (ones demonstrating early signs of buying intent) can focus their engagement efforts (and spend) on in-market accounts. For example, you might notice that many advisors at a particularly large firm begin downloading your ebook on topic X. Based on that insight, you could prioritize that account for more targeted sales outreach, asking them “can we help you learn more about topic X?”

You can, in effect, identify who wants to buy what, investing more resources of time and marketing spend on the winners and less on “prospects” who show no intent to buy from you right now. (Which can of course change quarter to quarter.).

To know which companies or teams are the winners, however, is the trick. You’ll want to start with a scoring model. Today, there are four broad areas of data you might consider leveraging to build your scoring model. You may already have some of this data (though it may be scattered across systems). With other data, you may have to purchase it. Not all are necessary, but the more data you have the more precise your account targeting and engagement will be.

Combined, this data gives you an enriched and timely view of who’s “in-market,” or searching for your offerings. Together, the four data types working together create the acronym “FIRE”:

- Fit—how well does a firm fit your requirements, and you theirs? (E.g. Are they low-risk?)

- Intent—how actively are they researching products like yours across the internet?

- Relationship—does your team have relationships with key leaders or investors there?

- Engagement—how actively are they visiting your web properties or engaging with your marketing and sales efforts?

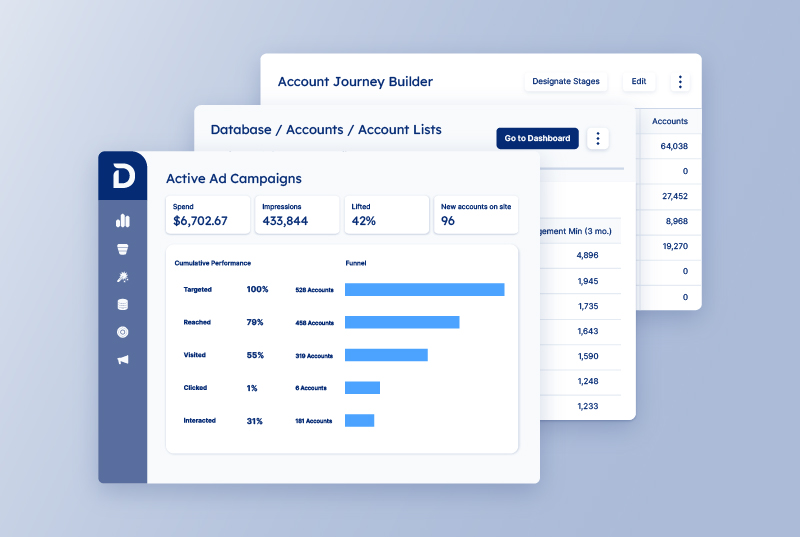

The engagement data often comes from your website, CRM, and marketing automation system. The relationship data will come from your sales team (or sometimes, a software like LinkedIn). The fit data will come from a scoring model that you either develop yourself (a fitness rating system of 1-5 stars is enough to begin) or obtain through a platform like Demandbase, which calculates it for you using machine learning. Finally, intent data—the most sought-after of the bunch—is something you purchase from an intent data provider. (Also available through Demandbase.)

Identify what you already have in the way of Fit, Relationship, and Engagement, and then engage with an intent data partner who can help fill out the rest of your “account picture.” That visibility provided by account intelligence gives your financial services organization the digital-first capacity to (1) identify and sense customer needs as they evolve and (2) respond to those “intent signals” by personalizing engagement at the account level, so you can address those evolving account needs with timely, relevant solutions.

Use your intent provider to scan the known universe

In the case of data, “Intent” means “a presumed intent to buy.” It is an indication that prospective clients or decision-makers within companies who might buy have taken actions somewhere online that reveal their intention.

The providers pick up on those far-flung digital activities in a network of data sharing. There are several such groups, Demandbase being one of them. It works like this:

- Buyers conduct research online, on ratings agency sites, lender comparison sites, and publications like The Wall Street Journal and Yahoo!

- Those publications send privacy-safe data to intent data providers.

- Intent data providers use machine learning and artificial intelligence to figure out and uncover which visitors work at which firms or companies.

- Buyers of intent data can “enrich” their existing list of accounts with real-time data on which ones are looking for, say, commercial loan products like theirs.

- Buyers of intent data can also combine this with their website Engagement data to “unmask” some anonymous website visitors, thus expanding the volume of known leads they can engage with and potentially convert to revenues.

With Intent data, you can pull a list of companies that match your criteria—Fit, Relationship, and Engagement—and are also exhibiting intent to buy—Intent. A bank looking to market particular financial products could use this to shorten their list to just those companies who are both a fit and are showing buying intent, and focus their efforts there.

When you allocate more of your resources on the accounts most likely to purchase, you get more bang for your buck. Accounts that realize that you understand them and what they need are also more likely to develop strong relationships with you based on shared value. Again, engaging with accounts you know something about is far better than using generic engagement playbooks and sandwich boards that say, “choose me!”

Instead of “me too” marketing, focus your engagement efforts on a group of companies that exhibit every indication of being good buyers (low risk, high-yield) and of being interested in products like yours. It’s a level of insight most financial services sales teams are unaccustomed to, and you can use it to launch an account-based pilot program that will get (and prove) success.

So begins your digital transformation

Pouring more resources into fewer, higher-value, and interested accounts pays off by enabling you to generate more revenues/ROI with less spend, helping establish your team as a center of excellence. You can also help lead your company’s digital transformation (best of all, you will have the data to prove it), and adapt to a world where everything about buying and selling has changed.

It doesn’t take the entire business’ approval to start. Just you, a pilot, and data about your buyers’ intent.

Related content

We have updated our Privacy Notice. Please click here for details.